District Lending: Breaking the Volume-Margin Trade-off

District Lending was founded in 2018 and operates in 14 states. Through a lead-purchase model, they’ve built a strong business converting internet leads with competitive pricing and efficient execution. Division President Josh Leary describes District as “always at the bleeding edge of technology” in an industry that often lags in tech adoption.

With eight loan officers, Leary had no interest in scaling headcount further; his goal was efficiency and margin, not empire-building. District generates 12-15K website visitors per month and has invested in AI automation to scale without adding staff.

Even with their success, District faced the same fundamental trade-off as every broker: offer sharp pricing to win more deals, or maintain strong margins on each loan. For a lead-based business like District, this generated constant tension. Internet leads go cold quickly, so speed and efficiency matter. But so does price, and so does margin. The standard model forces brokers to choose from among these value propositions. To reach rock-bottom pricing, brokers often find themselves working with wholesalers notorious for outdated and inefficient workflows that can lead to poor customer experiences and even jeopardize deals.

This fundamental economic tension notwithstanding, District performed well under the traditional wholesale model, earning roughly $3K per file at competitive pricing. But there was an immutable ceiling on their economics.

When Leary heard from an industry contact that Pylon was promising direct access to Wall Street rates, he thought of the additional margin this could unlock on every loan. While Pylon’s rates sounded almost too good to be true, he decided it was something worth evaluating. If early adoption could give him a competitive advantage, he didn’t want to miss the chance to get in on the ground floor.

Why Pylon

Leary had two key evaluation criteria: whether Pylon’s rates could consistently beat his existing wholesale rates, and whether Pylon’s all-in-one software could match or even outperform his existing tech stack. District was using Arive as their LOS and POS and LoanSifter as their PPE.

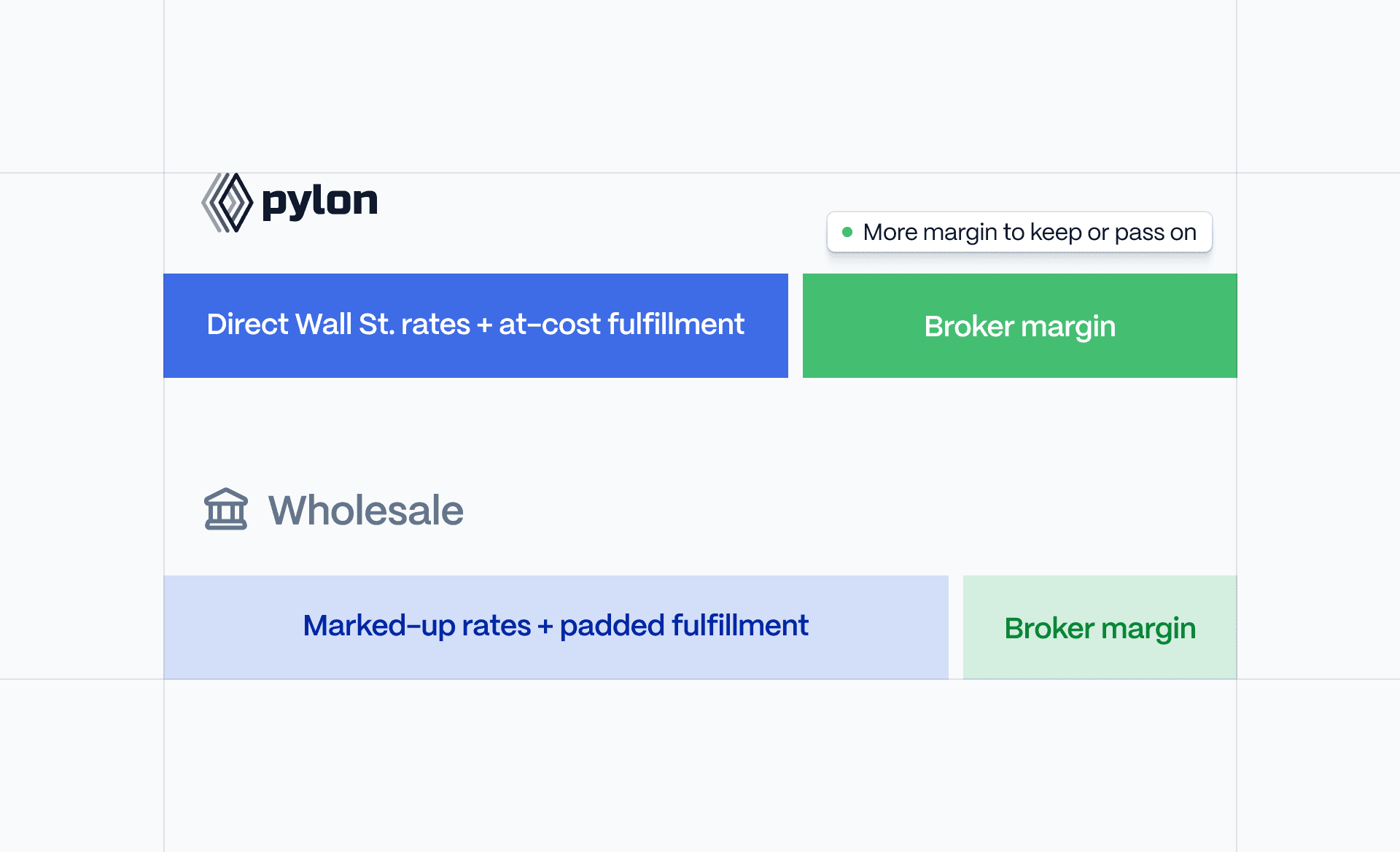

Pylon is more than just another wholesale lender; it’s an entirely new paradigm combining the fulfillment of a wholesaler with all the functionality of an LOS, POS, and PPE, plus more. By replacing wholesalers’ costly mortgage factory model with our AI-native mortgage rails, we’re able to give brokers direct access to direct Wall Street pricing without the 75-200bps wholesale markup.

The evidence on pricing appeared immediately. When District compared Pylon to their rates in LoanSifter, Pylon consistently unlocked 80%+ greater margin at identical note rates. And unlike discount wholesale lenders notorious for outdated technology, Pylon promised to deliver greater operational efficiency by automating most of the origination process (disclosures, underwriting, order-outs, etc.) in addition to LO workflows.

Leary made the decision to implement Pylon and give it a chance to perform in the real world.

Implementation

Within days of signing up, District went live with Pylon. The onboarding process was standard: paperwork, compliance documentation, and approval workflows. Leary noted that the biggest implementation lift was a shift in thinking.

“Pylon isn’t another wholesale lender. It’s a new paradigm that consolidates both the wholesaler and the software stack into one lower-cost, margin-generating platform. So we needed to think about Pylon differently to maximize its value.”

District began using all five components of Pylon’s platform:

- Elements – Borrower-facing portal

- Command Center – Loan officer tooling

- Capital – Wall Street rates and funding

- Decisioning – Automated underwriting

- Compliance – Disclosures and documentation

Pylon soon became the default solution in District’s workflow. Roughly 80% of District’s conventional volume now runs through Pylon, while they still work with wholesale lenders for certain loan types such as non-QM that Pylon doesn’t support yet (but will soon).

Economic advantages

For District, loan economics have always been the first consideration when evaluating any new partner. According to Leary, “At the end of the day, it’s about winning more deals and making more money. Everything else is secondary.”

Since launching Pylon, District captures an average of $2,500 in additional margin per loan while maintaining the same highly competitive borrower pricing.

Prior to Pylon, strong borrower pricing typically yielded about $3K in broker compensation. With Pylon, identical pricing now yields more than $5K.

As Leary explained: “If you go to Pylon and make $3K on the deal, you’re on another level of crushing competitors on pricing. So brokers can decide whether to pass that value to borrowers or capture it as margin, or a little bit of both. With Pylon pricing, deals close.”

The industry’s persistent trade-off between low rates and strong margins no longer has to dominate broker economics.

Operational advantages

Beyond economics, Pylon delivered a number of major operational improvements for District:

- Instant disclosures – While traditional portals often take 2-3 days to generate disclosures, Pylon typically delivers them immediately.

- Automated order-outs – Following approval, Pylon automatically orders appraisals and title without manual intervention.

- Reduced processor dependency – Automation reduces the need for dedicated processors. Loan officers can clear conditions and task items directly to borrowers.

- Software-powered underwriting – Pylon’s decisioning engine typically delivers credit evaluations in an hour or less.

- Close in 15 days – As a result of Pylon’s operational efficiencies, District consistently closes loans in about 15 days.

The paradigm shift

As Leary observed: “Insane pricing and insane tech are two worlds that just don’t meet. But with Pylon, they do.”

The mortgage industry has long operated on fixed trade-offs: discount wholesalers deliver low rates but force brokers to deal with their outdated tech and workflows. Premium wholesale platforms operate efficiently but have higher pricing. Brokers choose between better pricing and better margins, while maintaining a separate software stack outside of their wholesale relationships.

Pylon eliminates these constraints. By replacing the traditional “mortgage factory” model with mortgage rails, Pylon operates at a fundamentally lower cost structure, enabling institutional pricing to be passed directly to brokers. At the same time, our best-in-class software platform increases LO efficiency by as much as 3x compared to traditional LOS-POS-PPE workflows.

Looking forward

District is monitoring Pylon’s roadmap for several capabilities that will unlock additional efficiencies:

- Borrower self-service for rate locks and disclosure generation

- Instant conditional approvals without loan officer review

- Full product coverage including government and non-QM loans

Long before Pylon, Leary was moving District in the direction of a true self-service borrower experience—citing Better as the industry’s current north star. Pylon’s roadmap will make that vision achievable for District while at the same time unlocking economic advantages they previously couldn’t access.

About District Lending

District Lending is a technology-forward mortgage brokerage founded in 2018. Based in Paradise Valley, Arizona and operating across 14 states, District combines personalized service with innovative technology to deliver exceptional experiences for borrowers who value both speed and rate.