The broken capital model of mortgage

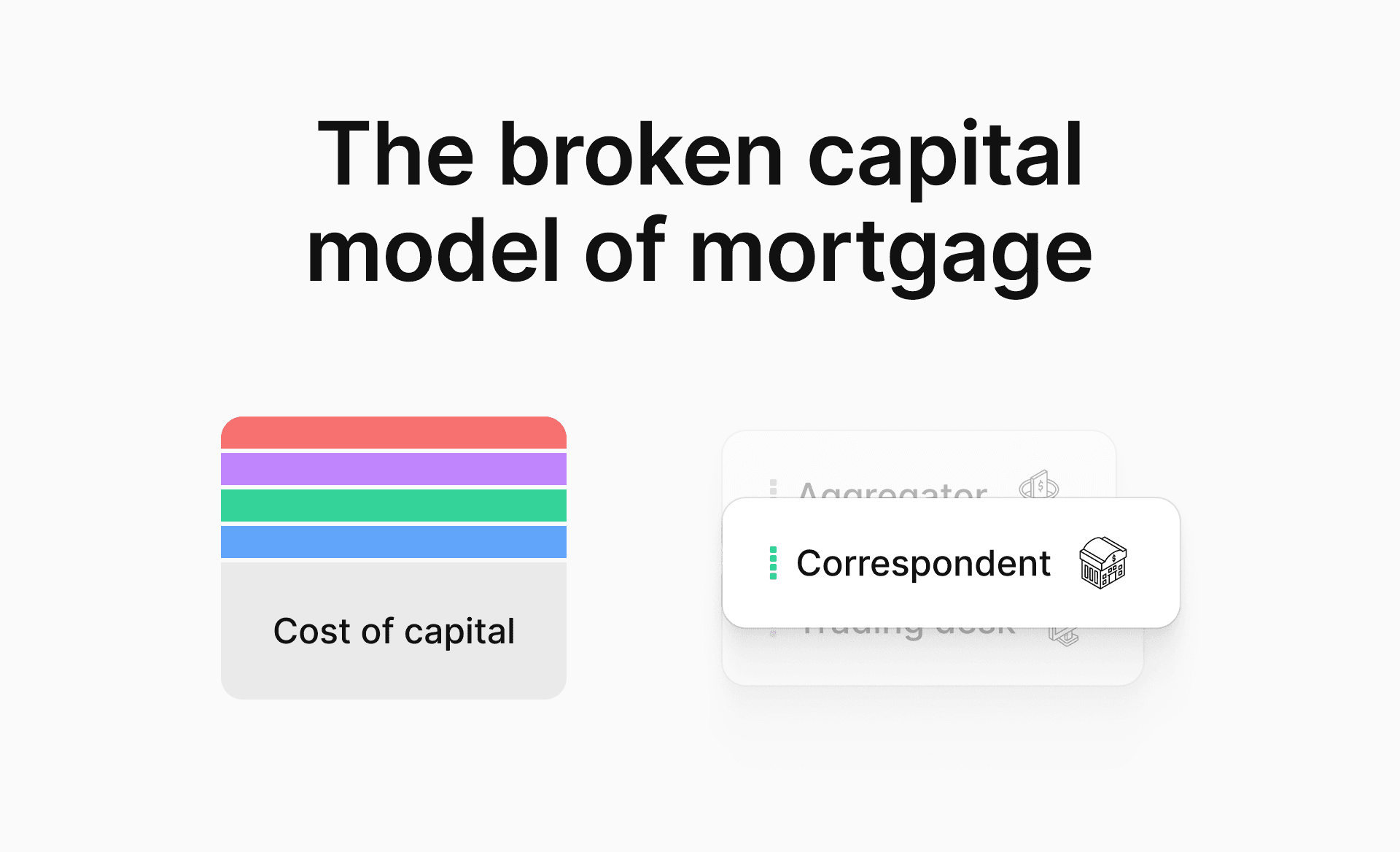

In between mortgage originators and the institutional investors who ultimately buy their loans, there’s a chain of intermediaries.

Originators sell closed loans to an aggregator or correspondent investor. The aggregator sells whole loans onward to a bank’s correspondent channel or pools them for securitization through a trading desk. The economics ultimately flow to the pension funds, insurance companies, hedge funds, and other institutional buyers that hold mortgage exposure.

Brokers encounter an additional layer: their wholesale lender.

For some originators the chain is shorter. For many it’s longer. Each link is an independent business with its own operating costs, hedging costs, and required return, and each one layers those costs onto the rate sheet.

The cumulative markup is often between 75-200 basis points.

This figure isn’t operating margin alone. It covers each layer’s hedging costs on the gap between funding and pool delivery, loss reserves against loans that fail eligibility and have to be sold on the scratch-and-dent market at a discount, rep-and-warrant capital, and required return.

None of these components are visible to originators, who have no way to determine whether uncompetitive pricing is because of borrower characteristics or because their wholesaler or aggregator is pricing wider that week. They build margin into the next quote to absorb the uncertainty, and the borrower pays for that too.

Why capital layers exist

The capital model of mortgage wasn’t always as layered as it is now. Before 2008, the structure was different: banks held more loans on their own balance sheets, and the post-crisis pullback from direct retail origination at scale, combined with regulatory pressure on rep-and-warrant capital, drove the expansion of the intermediary layer into the form it takes now.

Within this structure, each layer has earned its place. Aggregators and correspondent investors bundle loans from many originators into volumes that institutional investors are willing to buy, standardize the pools to make them tradeable, and manage the rep-and-warrant risk that no single small originator can carry. Wholesalers give brokers a path to capital they can’t reach themselves. These margins are the price of doing the work that originators and investors can’t do themselves.

But this structure leaves originators exposed. When rates spike and markets become volatile, intermediaries’ hedging costs rise and they widen their markups to absorb the risk. Originators face the same volatility on their own book and find their pricing getting less competitive at exactly the moment their borrowers need them to be more aggressive. The intermediaries protect themselves first. Originators absorb the rest.

On its face, this system functions. It just doesn’t function well for originators.

One layer instead of several

While each intermediary does real work, the work doesn’t need to be spread across two to five separate businesses. Standardization, verification, bundling, investor matching, and capital markets routing can be done once, in one place, through software.

That’s where Pylon comes in. We connect originators directly to institutional investors, bringing the capital markets relationships we’ve earned by aggregating volume across every originator on our platform. A mid-sized broker or a fintech launching its first mortgage product get the same execution as a lender doing a thousand units a month, because investors are pricing against Pylon’s combined book.

Originators on Pylon see the price of capital directly from the institutional source. On top of that we take a small, transparent margin for the value we add: not only connecting originators to the capital markets, but also handling origination end to end and repping and warranting every loan.

On Pylon’s mortgage rails, originators can take back the 75-200bps that used to be the capital and mortgage manufacturing markup. They can use that recaptured margin to compete on rate, expand their margin, or both.